THE FINAL CHAPTER!

|

Should the government get involved? Why or why not?What are the benefits and drawbacks?

Consumerism is a social and economic order that encourages the purchase of goods and services in ever-greater amounts. Early criticisms of consumerism are present in the works of Thorstein Veblen (1899). Veblen's subject of examination, the newly emergent middle class arising at the turn of the twentieth century, comes to fruition by the end of the twentieth century through the process of globalization. In this sense, consumerism is usually considered a part of media culture. The term "consumerism" has also been used to refer to something quite different called the consumerists movement, consumer protection or consumer activism, which seeks to protect and inform consumers by requiring such practices as honest packaging and advertising, product guarantees, and improved safety standards. In this sense it is a movement or a set of policies aimed at regulating the products, services, methods, and standards of manufacturers, sellers, and advertisers in the interests of the buyer. In economics, consumerism refers to economic policies placing emphasis on consumption. In an abstract sense, it is the consideration that the free choice of consumers should strongly orient the choice what is produced and how, therefore the economic organization of a society (compare producerism, especially in the British sense of the term). Also this vote is not "one man, one voice," but "one dollar, one voice," which may or may not reflect the contribution of people to society. --------- Keeping up with the Joneses - refers to the comparison to one's neighbor as a benchmark for social class or the accumulation of material goods. To fail to "keep up with the Joneses" is perceived as demonstrating socio-economic or cultural inferiority. See all handouts below.

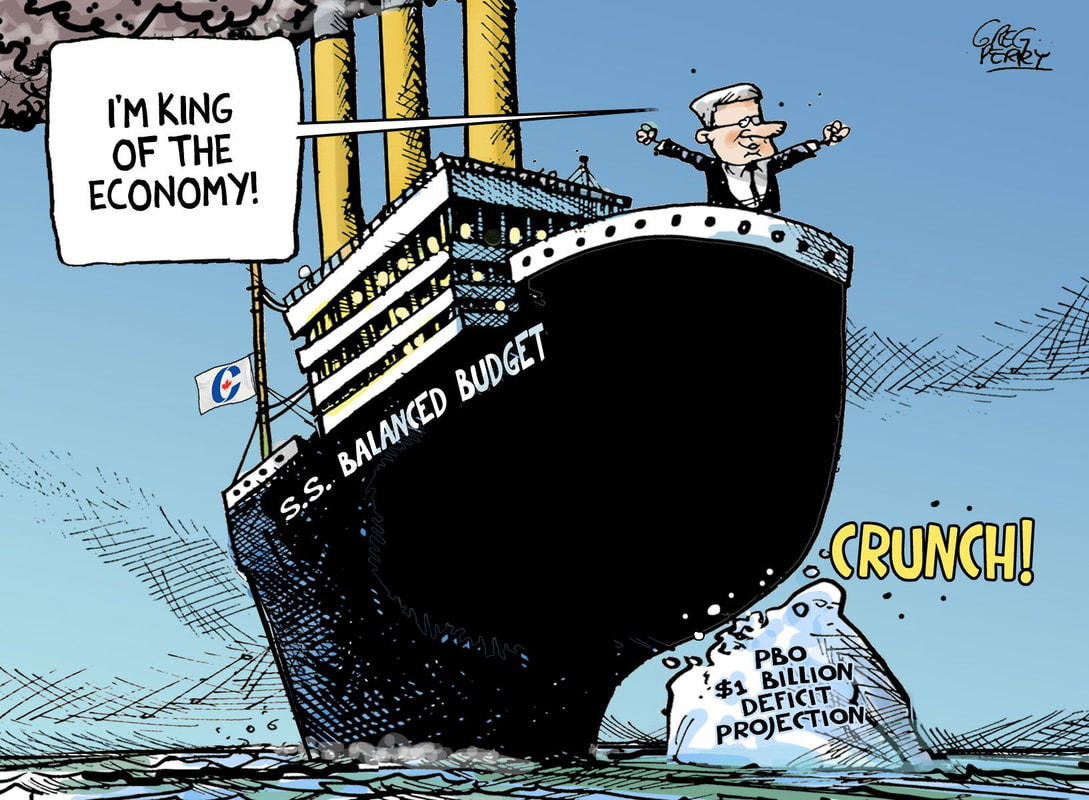

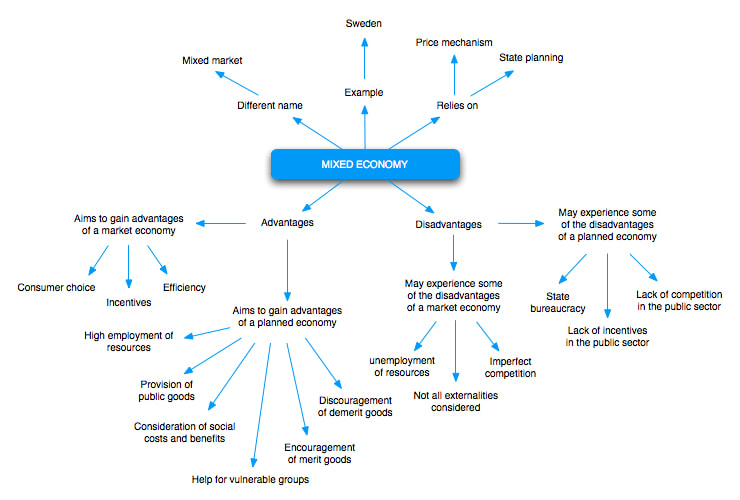

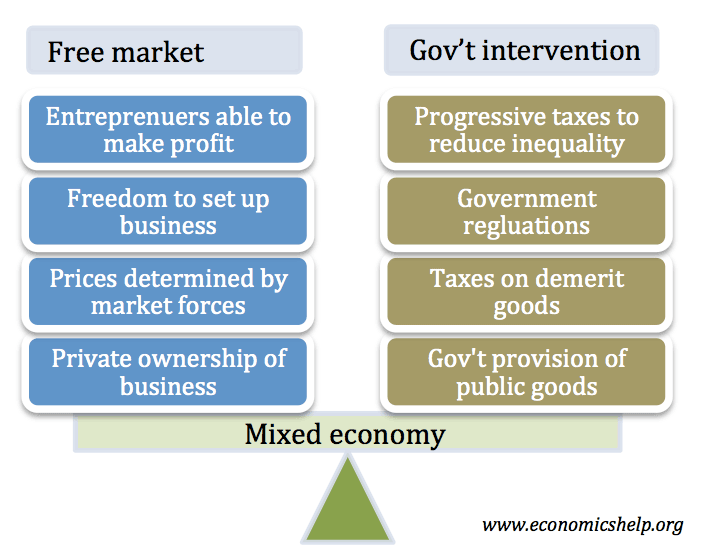

Look at imagery (what does the boat represent?), who is speaking? What does he mean? What is the significance of the iceberg? How does this relate to the 2008 financial crisis? What is a budget? What is a deficit? And for your musical entertainment (and a serious hint...) watch the video below.  Below are two videos... the first in on a MONOPOLY (no, not the game) and the other is on the 2008 financial crisis and why it happened. Both are relevant for the upcoming Chapter 6 test. Ontario Premier Kathleen Wynne announced yesterday that the province’s minimum wage will climb to $15 an hour on January 1, 2019. It currently stands at $11.40 an hour. The move will affect the close to 12 per cent of Ontario workers who earn minimum wage, as well as all facets of the economy linked to their labour. Reaction to the news was vehement and polar. Proponents argue the measure is necessary to match inflation and rising costs of living, while opponents suggest such a drastic increase hurts business. Plenty of research has determined that wage increases for society’s bottom earners is positive. According to a 2006 statement co-signed by over 650 economists, including 5 Nobel prize winners and 6 past presidents of the American Economic Association, “a modest increase in the minimum wage would improve the well-being of low-wage workers and would not have the adverse effects that critics have claimed.” But this is not a modest increase – we’re talking about a 31 per cent raise almost from one year to the next. Without a reliable case study to draw from, speculation on the measure’s ramifications is high and heated. Falling somewhere between the guy who posts “dumb ass Liberals” on all of our Facebook articles and a Nobel prize-winning economist, we’ve outlined some of the pros and cons of a $15 minimum wage in Ontario… Pro: More purchasing power for low earners Annual inflation (how much things cost from year to year) in Canada over the past eight years has totalled 11.25 per cent, while the minimum wage in Ontario has increased by just 8 per cent during that time. This offset has made it harder for people in the province’s lowest income bracket to pay for basic necessities, let alone afford property. The most obvious benefit of a higher minimum wage is that it puts more money in the pockets of those who need it most. Con: It will propel inflation Inflation is kind of like the white whale in Moby Dick in that as soon as you try to catch it, it makes a move to evade being caught. Ontario’s bottom earners may see a small window of increased purchasing power before a considerable increase in the price of consumer goods. Businesses will pass the burden of balancing increased wages with their bottom line onto you, the customer, by charging more for their products. Manitoba, for example, has decided its minimum wage should increase annually at the rate of inflation. Pro: An economic boost More purchasing power, lower employee turnover, less dependency on government welfare programs, easier recruitment, and higher employee productivity are all economic stimulants derived from a sizeable raise in income. This argument follows the you gotta spend money to make money principle. Small business owners, despite what we’re about to say in the following paragraph, should understand that a healthy economy is essential as they cannot export their way out of recessions. Con: It will hurt small businesses That higher wages will kill profits, cut jobs and slow growth is the crux of every argument by opponents of a higher minimum wage. Many small businesses cannot afford to incur additional costs without an immediate return, and could be forced to shut down or relocate to another province. Those leaning towards the more “medium” size might even consider moving abroad or outsourcing their labour. Pro: Reduces income inequality As in most of the developed world, income inequality in Canada is rising at an unprecedented rate. Kevin O’Leary will tell you that the two richest Canadians having as much money as the country’s poorest 30% combined is fantastic; that the money will “trickle down.” Except it doesn’t – it gets lost somewhere in a Cayman Islands bank account. More money for those at the bottom, who spend it at businesses who mostly employ minimum wage workers, keeps cash flowing within the lower and middle class. Con: Less hours, more burnout The reality is large companies with corporate responsibilities won’t put the interests of bottom-rung employees before their bottom line. An increased minimum wage will likely see less hours for those earning it while their workload is distributed among higher-salaried employees. And the last thing we need is more part-time work. So, small businesses don’t have money for higher wages; while the profits of large businesses are, unfortunately, first and foremost owed to shareholders and investors and not employees. Pro/Con: Accelerating the shift towards automation The robots are coming – and they’ll arrive a hell of a lot faster if companies are going to be forced to pay low-skilled workers $15 an hour. According to Washington-based public policy research organization Brookings, “if the price of labor rises too quickly, businesses have a bigger incentive to replace human labor with automation technology.” And you can be sure $15-an-hour workers aren’t building robots, so there’s no silver lining there. History has shown, however, that new industries have replaced those phased out by automation – consider the Industrial Revolution after the agricultural era. These new industries will possess their own demand for low-skilled, low-wage (albeit $15 an hour) work. Robots won’t just “take” our jobs, but automation will certainly re-calibrate them. One can speculate how an increased minimum wage accelerates this shift, though not in any quantifiably positive or negative capacity. One thing is certain: there is no consensus among experts if a significant increase in the minimum wage is objectively good or bad. What is clear, however, is that the most effective increases should be incremental (in tandem with the rate of inflation) as not to invite rash economic shifts.  A mixed economic system is an economic system that has a combination of a market economy, allowing for the private ownership of capital, and a command economy, which government intervenes to protect the public interest. Detailed Explanation:A mixed economic system blends characteristics of the command and market economic systems. Some governments, like the United States, have a bias in favor of a market economy, but the US’s government still imposes regulations and has a tax structure to try to redistribute income to the poor. Other countries, like China, lean toward the command economy, but during the past two decades the Chinese government has stepped up efforts to encourage private investment. There are two types of mixed economies: In one type the ownership of the means of production i.e., farms and factories is owned and controlled by the private sector and the Government merely controls and regulates the functioning of the private sector. In the second type the government directly participates in productive enterprise side by side with private enterprise. The government sets up industries of its own and invests its own capital and purchases or hires the productive resources and takes the risk of profit or loss like an ordinary entrepreneur. There are also Joint Sector which is shared both by Private and the Public Sector. The U.S.A. and the U.K. are prominent examples of first type of mixed economy while India represents the second type of mixed economy.

Here is Chapter 6 from the textbook and the workbook that accompanies it.

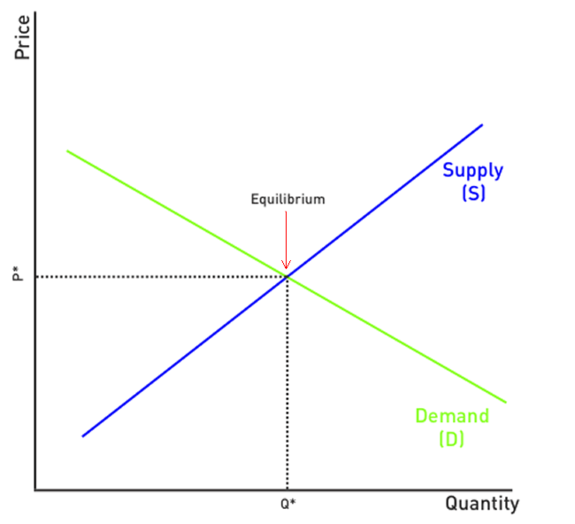

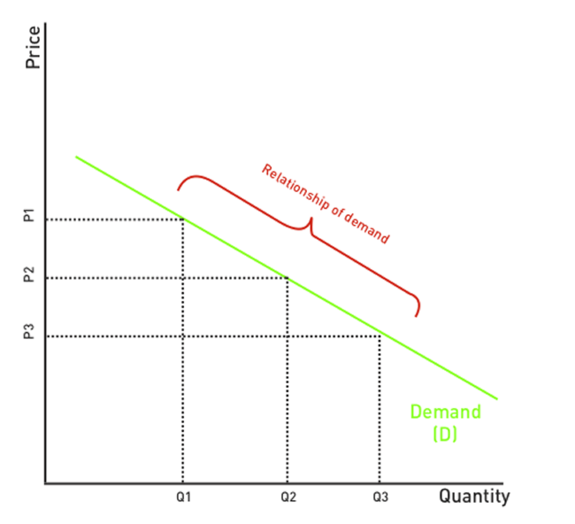

Supply And Demand In the context of supply and demand discussions, demand refers to the quantity of a good that is desired by buyers. An important distinction to make is the difference between demand and the quantitiy demanded. The quantity demanded refers to the specific amount of that product that buyers are willing to buy at a given price. This relationship between price and the quantity of product demanded at that price is defined as the demand relationship. Supply is defined as the total quantity of a product or service that the marketplace can offer. The quantity supplied is the amount of a product/service that suppliers are willing to supply at a given price. This relationship between price and the amount of a good/service supplied is known as the supply relationship. When thinking about demand and supply together, the supply relationship and demand relationship basically mirror each other at equilibrium. At equilibrium, the quantity supplied and quantity demanded intersect and are equal. In the diagram below, supply is illustrated by the upward sloping blue line and demand is illustrated by the downward sloping green line. At a price of P* and a quantity of Q*, the quantity demanded and the supply demanded intersect at the Equilibrium Price. At equilibrium price, suppliers are selling all the goods that they have produced and consumers are getting all the goods that they are demanding. This is the optimal economic condition, where both consumers and producers of goods and services are satisfied. The Law Of Demand Very simply, the law of demand states that if all other factors remain constant, if a good's price is higher, fewer people will demand it. As the price of that good goes down, the quantity of that good that the market will demand will increase. In the diagram below, you see this relationship. At price P1, the quanity of that good demanded is Q1. If the price of this good were to be decreased to P2, the quantity of that good demanded would increase to Q2. The same is true for P3 and Q3. When prices move up or down (assuming all else is constant), the quantity demanded will move up or down the demand curve and define the new quantity demanded. The Law Of SupplyAfter understanding the law of demand, the law of supply is simple, it's effectively the inverse of the law of demand. The law of supply states that as the price rises for a given product/service, suppliers are willing to supply more. Selling more goods/services at a higher price means more revenue. In the diagram below, you can see that as the price shifts from P1 to P2, the quantity supplied of that good shifts from Q1 to Q2. The movement in price (up or down) causes movement along the supply curve and the quantity demanded will change accordingly.   As a novice, economics seems to be a dry social science that is laced with diagrams and statistics; a complex branch that deals with rational choices by an individual as well as nations — a branch of study which does not befit isolated study but delving into the depths of other subject areas (such as psychology and world politics). What is Economics?Economics Definition: Economics is essentially a study of the usage of resources under specific constraints, all bound with an audacious hope that the subject under scrutiny is a rational entity which seeks to improve its overall well-being. Two branches within the subject have evolved thus: microeconomics (individual choices) which deals with entities and the interaction between those entities, while macroeconomics (aggregate outcomes) deals with the entire economy as a whole. A typical college student (or an overburdened husband?) appreciates the lessons of economics in day-to-day life. Semester books and carton of cigarettes (choices) are to be purchased with a limited amount of pocket money (constraints). The aim of studying economics is to understand the decision process behind allocating the currently available resources, the needs always unlimited but resources being limited. Adam Smith wrote ‘An inquiry into the Nature and Causes of the Wealth of Nations‘ which as the name suggests, was an attempt at understanding the reasons behind the economic growth (or lack thereof) of a nation. An interesting backdrop to consider here — the fundamental assumption that we need to make for the whole economic system (as we know it today) to work is that human beings are motivated by pure self-interest and will take decisions that they think will make them ‘better off’ now or sometime in the future. The economic and political systems of a country are closely inter-linked and jointly determine the well-being of its citizens. Economics Basics – Demand & SupplyIt is perhaps one of the most fundamental tenets and provides a fundamental framework in which to assess the actions of an economy. Definition of Demand: Demand is the quantity of a good (or service) the buyers are willing to purchase at a particular price. Definition of Supply: Supply is the quantity of a good the sellers are willing to deliver at a particular price. Meanwhile price is a result of the constant tug-of-war between the demand and supply. And all other random things kept constant for a good (brand, quality etc.); higher the price— lower will be the demand from the consumer (to save up for other purchases). Higher the price, higher will be the supply from the manufacturers (make hay while the sun shines!). The former is called the law of demand, and latter is called the law of supply. Time also plays a huge role in a free-market economy, more so in the case of entities in a competition to serve the consumers. Stock-outs are no good for a supplier as it affects the brand and the consumer can move elsewhere. If there is an excess of demand, the producers have to gauge the nature of demand first (seasonal, increasing trend) to react in a swift fashion, to corner the market and retain the existing customers. The stable state of equilibrium in an economic system makes the economy efficient, the suppliers are moving their goods and the consumers are getting what they are demanding. The only point worth noting: the point of equilibrium is ever-elusive and fluctuates like a wild boar in each minute quantum of time. Economics Basics – The free market hypothesis In a perfect free market, for any good or service— the total quantity supplied by the sellers and the total quantity demanded by the buyers will reach a state of economic equilibrium over time. Things closely follow the free market paradigm if two basic assumptions hold true: perfect competition and absence of “unnecessary” government quotas and regulations. Perfect competition assumes that no seller is large enough to sway the natural movement of the market owing to its large market share and cash reserves, which too often becomes the case for corporations in a capitalistic system with the wherewithal to wipe out smaller players. In these cases, regulations to prevent monopolies and unfair practices become all the important to ensure that the market remains efficient. On the other hand, too many government regulations and quotas (pre-liberalization India was on the verge of bankruptcy) hinder the natural process towards equilibrium and result in easily avoidable inefficiencies in the system. How much government regulation is the right amount is a question which we are yet to answer with full confidence, but we know for sure that both extremes can be really bad! Economics Basics – Cost, efficiency and scarcity

The ‘specialist world’The fundamental concept which is responsible for economic growth as we know it is specialization of labor. If an entity is really efficient in producing a commodity (output to input ratio is high), it has an advantage over another entity which is not that efficient in producing the commodity under consideration. If I am good at making shoes and you are good at making jam, it makes sense to do what we are good at and trade afterwards. Moreover, the economies of scale prove to be an icing on the cake — the production cost per unit decreases as we produce more and more of the same units (the initial one-time setup cost can be a major part of the total expense). And the best part is that both parties are better off after doing the transaction (and so is Mother Earth, for less wastage). Just to appreciate the grandeur of this simple idea, just imagine your standard of living in a world where you have to produce everything for yourself. You would likely revert to a medieval lifestyle, growing your own food and defending our own property. Say goodbye to the iPhones, cushy jobs, roads (even the shitty ones), branded clothes and the air-conditioned comforts. Studying economics can be both rewarding and intimidating at first, but knowledge of basic economics is essential not only for the B-School junta but for anyone who interacts with markets. In an era where having money is one of the prime determinants of the ability to make more of it, you better watch out and get your basics right. |

AuthorMr. Burt... social and English teacher. Archives

June 2018

Categories |

||||||||||||||||||||||||||

RSS Feed

RSS Feed